Inflation became a problem in 2021, and the Fed has raised interest rates to combat it. The economy went into a brief recession last year but recovered quickly. Now, in 2023 several mid-size banks failed. What does it all mean? Are we in trouble or are these one-offs? Are we in for a “soft-landing” as Fed Chairman Jerome Powell has promised or is it a rocky road ahead?

I don’t write for Forbes or Money magazine, but one doesn’t need to be a so-called expert to understand something of finance. Reliance on experts who are often dishonest and use their positions to mislead the populace is a growing problem (especially today, more than ever). Draw upon your experience and knowledge, discern who is telling the truth and who is not. Many relied solely on government medical experts for COVID advice, and look where they landed us. Government experts made numerous mistakes and led to an unnecessary 10 year depression, a period wracked with the absolute wrong decisions from two different political administrations. You can do at least as well as they.

A skeptic generally does better than one blindly trusting the experts, who often don’t care about you or are not so good at their jobs. Below is my layman’s analysis, complete with geeky charts, but in terms all of us should understand. I think despite happy talk from Washington, we are probably in for rough times ahead.

Government Spending

Recent economic problems can be linked to government spending. Money is like any other commodity; supply and demand for it fluctuates. As the US budget grows, the Treasury prints more money to cover its expenses (i.e. the supply of money increases). As the supply of money increases, its value decreases. This is no different than the decrease of gas prices during an oil glut. As the value of a dollar declines, businesses charge more for goods to make up for the loss in the value of dollars they receive. Voila: inflation. In summary:

- more government spending -> money supply increases -> value of money decreases->businesses charge more to make up loss of “real” dollars->inflation

The great Milton Friedman, put it this way forty-five years ago:

“Inflation is made in Washington because only Washington can create money,” Friedman said in a 1978 lecture that has gained currency again on social media. “It’s always and everywhere a result of too much money, of a more rapid increase in the quantity of money than in output. Inflation in the United States is made in Washington and nowhere else.”

It reminds me of the nursery rhyme.

K-i-s-s-i-n-g! (spell it out)

First comes love.

Then comes marriage.

Then comes baby* in the baby carriage,

First comes government spending, then inflation, and then the Federal Reserve intervenes. In 2023, what comes next is likely recession.

The Federal Reserve has two mandates: price stability (preventing inflation or deflation) and maximizing sustainable employment (i.e. limiting unemployment). Let’s focus on inflation. The Federal Reserve seeks to reverse the inflationary factors listed above. They raise interest rates (specifically, the Federal Funds rate) which decreases the demand for money which increases the dollar’s value which means businesses stop raising prices and inflation is slowed.

Higher interest rates mean fewer seek to borrow (i.e. the demand for money decreases), and the value of the more limited supply of money increases. Inflation, which is often characterized as “too much money chasing too few goods” is brought under control as overall consumer spending decreases. However, as consumer spending decreases, businesses sell fewer goods; some go out of business and lay off employees. In other words, interest hikes can lead to recession.

Inflation/Interest Rates

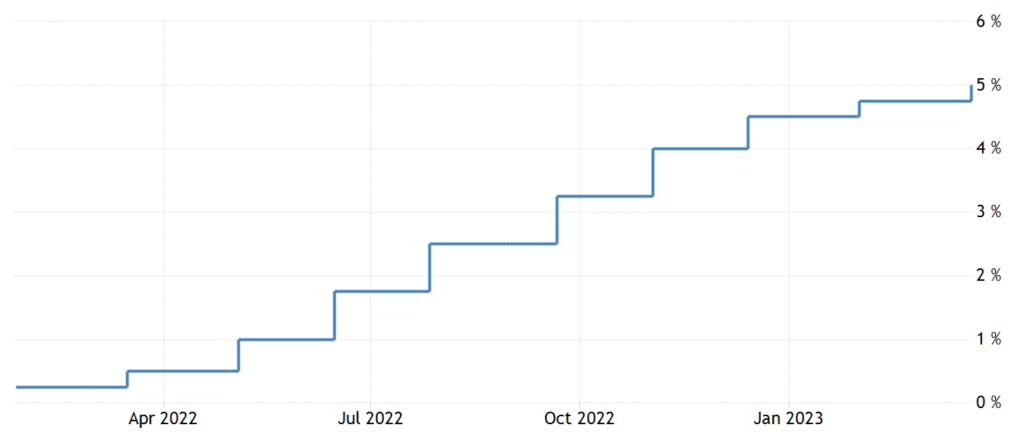

Current Federal Reserve Chairman Jerome Powell apparently believes he can fine tune the economy, increasing the interest rates at just the right pace, to provide a proverbial “soft landing”. The Fed has a goal of a 2% annual inflation rate. We have wildly missed that target since 2021. In 2022, the Fed raised rates in an effort to tamp down inflation.

https://www.reuters.com/article/usa-fed-powell-soft-landing-idUSW1N32Z02Q

Federal Reserve Chairman Jerome Powell said on Wednesday . . . it’s still possible the economy may not face a sharp downturn as the Fed works to contain inflation.

In terms of a soft landing for the economy, “There’s a pathway to that and that path still exists,” Powell said at his news conference following the Federal Open Market Committee meeting.

Powell is a powerful figure and has great control over the economy. Many say the Fed Chairman is more influential with regard to the economy than the president, although the president generally gets the credit or blame for the economy. However, I wonder if Powell is really the expert so many think he is. Is he walking this tightrope precisely or is he bowing to political pressure not to put the economy into a recession before the presidential campaign heats up (the first caucus is just ten months away)?

Senator Elizabeth Warren who may still have aspirations to the presidency herself is not pleased with Powell’s tinkering of the rates. She thinks he is moving too fast:

Sen. Elizabeth Warren (D-Mass.) stepped up her criticism of Federal Reserve Chairman Jerome Powell following the Fed’s most recent interest rate hike Wednesday, saying that he is a “dangerous man” to serve in his role.

Warren told CNN’s Jake Tapper in an interview that Powell is doing a “terrible job” in his position and is risking sending the economy into a recession with the Fed’s continuous interest rate increases.

However, Powell, has, in fact, been circumspect in raising rates the past twelve months. The Fed’s hesitation on these rate increases can lengthen or exacerbate our existing problems. In the late 1970s, then Fed Chairman, Paul Volcker, aggressively raised rates to pull the economy out of the woes of “stagflation”. Volcker took the rates up to 20%, four times what they are today. Mortgage rates went to 18% in the 1980s as well.

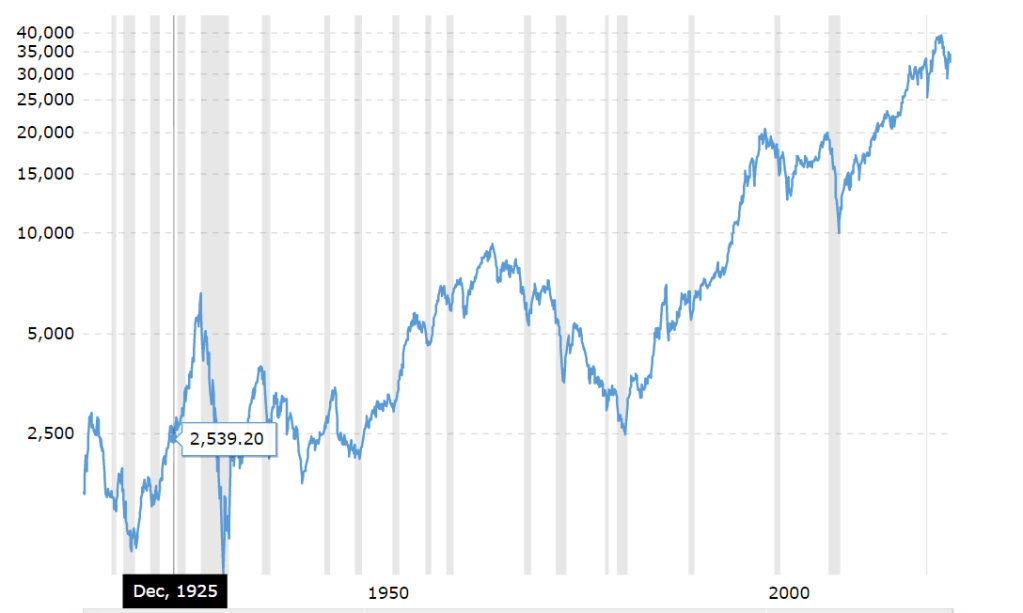

The economy reacted to the Volcker interest hikes and went into a recession in 1981, the first year of President Reagan’s first term. Reagan’s party lost big in the 1982 mid-terms because of the poor economy (minus 26 house seats and four senate seats). However, by 1984, the economy was booming again and Reagan won 49 states in his re-election bid. What followed was the longest period of economic expansion in American history. Over the next 18 years, the US stock market increased 8-fold in value (after virtually no gain during the prior thirty years). This stretch was by far the market’s largest percentage increase ever.

Senator Warren blames Chairman Powell for raising rates too fast, but he is actually hesitant to raise rates. Is Powell ignoring the political implications or trying to placate them? His effort to execute a soft landing seems too cute for me.

Both Powell and Treasury Secretary Janet Yellen (the Fed Chairman before Powell) too said inflation was transitory in 2021.

Yellen-admits-she-was-wrong-about-inflation

Both Yellen and Federal Reserve Chair Jerome Powell repeated on several occasions last year that rising inflation was “transitory” in nature and that prices would return to normal as pandemic-related supply chain bottlenecks cleared — a prediction that has turned out to be woefully off the mark.

“I was wrong then about the path that inflation would take,” Yellen said during an appearance on CNN late Tuesday. “As I mentioned, there have been unanticipated and large shocks to the economy that have boosted energy and food prices and supply bottlenecks that have affected our economy badly that I, at the time, didn’t fully understand, but we recognize that now.”

As Maxwell Smart used to say: “missed it by that much”

Chairman Volcker did not hesitate and did not avoid the short-term pain: recession, staggering home interest rates, unemployment, etc., but the pain was short-lived and not all that painful when compared to the boom that followed. The folks running the economy today are too political and have not been proven right enough to suit me. Volcker’s (and Reagan’s) strategy should be considered more seriously by folks today.

Inflation has been a problem for two full years now. Both Powell and Yellen didn’t recognize the inflation initially, and now, after two years, they still want to soft-pedal. Larry Kudlow who has been a commentator on TV for ages, share his concerns below. Kudlow, by the way, served in both the Reagan and Trump administrations as economic advisor. He argues Powell is not focused enough on controlling inflation.

The Fed’s rate hikes has been inconsistent. This vacillation could land us in a longer recession. The Fed waited until 2022 to even raise rates. Even then, they kept rate increases low (0.25% increases), ramped up a bit mid-year, and have slowed again, nothing like the increases from the Fed in the 1980s. The Fed funds rate is now at 5%, a quarter of where they went under Volcker.

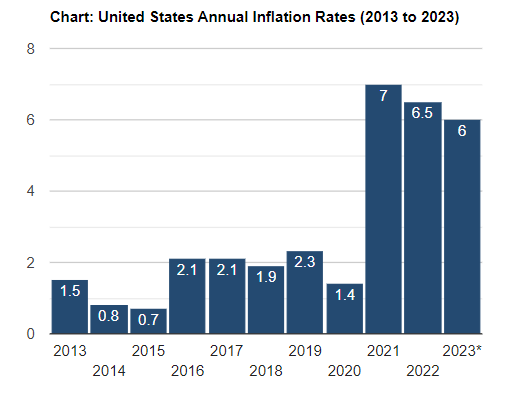

The soft landing of low inflation and continued economic growth is not yet apparent. Inflation remains high; it is still 6% the first two months of 2023. Before the last three years, 1990 was the last year the inflation rate rose above 6%. We have not had consecutive years above 6% since 1978-1981. I don’t get a warm and fuzzy feeling from the current numbers:

Other Problems

Ben Shapiro likes to say the economy was put into an artificial coma in 2020. The Biden administration could have literally done nothing and the economy would have roared back after COVID restrictions were lifted, but they had to tinker. The Trump administration began the out-of-control spending in 2020 with several (some unnecessary) COVID bailouts and the Biden administration continued them and added more pricy legislation like the Inflation Reduction Act, which has nothing to do with controlling inflation (and obviously hasn’t worked to control it). Government spending, the only source of inflation per Milton Friedman, skyrocketed:

| FY | DEFICIT (In Billions) | DEBT INCREASE (In Billions) | DEFICIT-TO-GDP RATIO |

| 2016 | $585 | $1,423 | 2.4% |

| 2017 | $665 | $671 | 3.4% |

| 2018 | $779 | $1,271 | 3.8% |

| 2019 | $984 | $1,203 | 4.6% |

| 2020 | $3,132 | $4,226 | 15.0% |

| 2021 | $2,772 | $1,484 | 12.1% |

| 2022 | $1,375 | $850 |

The budget deficit has exceeded $1 trillion the last three years. Previously, only 2009 and 2010 exceeded this threshold. President Biden’s budget for fiscal year 2024 doesn’t reverse trends. Let’s spend, spend, spend until Daddy takes the T-bird away. It is as we have become accustomed to deficit spending for so long that nobody is concerned:

WASHINGTON — U.S. President Joe Biden on Thursday unveiled a $6.8 trillion government spending plan for 2024 calling for dozens of new policy initiatives and higher taxes on corporations and wealthy individuals

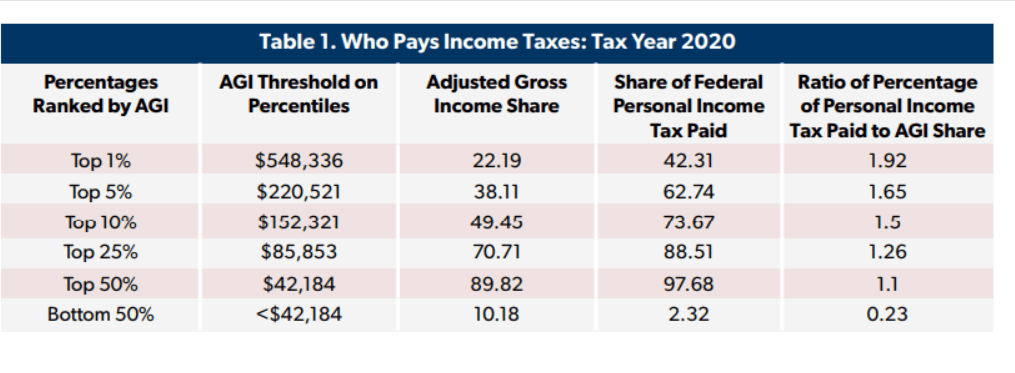

The Democrats always return to higher taxes for corporations and the wealthy; it is a political winner, but an economic disaster. The first problem with this strategy is that the wealthy already pay far more than their fair share. Three-quarters of all income taxes are paid by the top ten percent of income earners. The “tax the rich more” talking point is, and always has been, a lie. So, in order to achieve their targets, Democrats must tax more of the middle class; the term wealthy is redefined (although not openly) from millionaires to people like you and me.

The second problem is that government never decreases spending when revenues increase. More tax revenue encourages more spending, leading to the cycle of problems discussed above. Finally, more taxes, means less money for you and me to spend, and less money for our employers to spend on you or potential new employees as government crowds out the commodity market on dollars.

The economy grew at high rates in 1980s and 1990s, sparked by the Reagan tax cuts and reduction in government regulations. President Trump repeated this formula in 2017 and for three years the economy boomed again (reaching the highest GDP rates in more than 15 years).

The COVID shutdown stalled this recent boom for three quarters in 2020. Beginning in Fall 2020, the economy roared back, with the largest quarterly GDP increase ever. Again, increased government spending stunted this rebound. As can be seen, GDP declined for two quarters in 2020 and two more quarters in 2022 (the definition of a recession). 2023 has been a little better, but with more government spending and more taxes potentially on the way along with tepid Fed rate increases, we could be headed back into recession.

The long term problems are even more concerning than a potential recession. The US debt-to-GDP ratio is 107%, a level not seen since WWII. The national debt is an unfathomable $31 trillion. Neither President Biden nor former President Trump, currently the two leading candidates for their party’s nominations is even talking about this problem.

I would like to request from our political leaders: do not raise taxes and do not spend more money we don’t have. I am afraid the request is futile. Ay best, it only means a slight delay before falling off the cliff.

Social Security supposedly goes bankrupt in 2033 and Medicare in 2026. Social security used to be in a lockbox (saved for you when you retire), but the money taken from your paycheck today goes to a current retiree; it is not saved for you. Your future benefit will come from some future worker–if the program still even exists by the time you are eligible. We may still have time to fix all this, but no major political leader since former Speaker Ryan has made these programs an issue. Let’s hope someone finally makes this an issue. Otherwise, most of us will get nothing from these programs.

Banking

Bank failures were not a topic of concern before 2023, but became an issue when Silicon Valley Bank (SVB), a mid-sized bank became the largest failure in years. From the FDIC site:

SVB had a liquidity problem. The bank had invested heavily in Treasury bonds, a supposedly safe asset. However, the increase in interest rates, meant the bond values had significantly decreased. The 10-year treasury bond in March was paying near 4% for new investors, so earlier bonds (bought at the lower rate) had decreased in value. When bank depositors became concerned about the bank, they began taking their money out. The bank had to cover the withdrawals by selling its large portfolio of T-bonds at a big loss. They couldn’t cover the excess demands for cash and the bank failed.

There was an opportunity for a larger bank like Bank of America or Wells Fargo to step in and buy SVB, but the Biden Administration did not allow this initially, so the US government assumed responsibility to bail out depositors. The FDIC is supposed to cover the first $250,000 of a depositor’s account when a bank fails, but the FDIC is covering SVB depositors for far more. An ordinary Joe like me asks: why? The depositor is supposed to take the risk for the balance above $250K. If you make a risky investment, shouldn’t you, not the taxpayers, assume the burden of that loss? I thought the Democrats were looking out for the little guy, not for multi-million dollar investors. If everyone believes the government will bail them out no matter what, what stops banks from taking unnecessary risks that eventually burdens the taxpayers? Bank managers can take a wild risk and may strike it big, but if they fail, they do not need to accept the full consequences. Say what?

Secondly, bank investors, the ones that purchased stock in the bank, weren’t bailed out. They lost everything as stock values fell to zero. That’s interesting. Government covered large multi-million dollar depositors, but didn’t cover those who invested in the bank; those investors might include little guys like you and me who purchased bank stocks in their 401Ks.

A more consistent government policy is needed here.

The foreign bank Credit Suisse failed in March as well. They were bought up by the Swiss Central Bank. Is the problem spreading?

Another US bank, Signature Bank, failed also. Barney Frank, former Congressman and author of the oft-quoted and over-rated Dodd-Frank legislation was on the Board of Trustees for this bank. So much for his prowess in managing the economy; he can’t even manage one bank. The Dodd-Frank bill didn’t allow that banks such as SVB would be without a Risk Manager for eight months. Legislation doesn’t think of everything, but it does create a lot of unnecessary paperwork and restrictions along the way.

Laura Izurieta stepped down from her role as CRO of SVB Financial Group in April 2022, and formally departed the company in October, according to an SVB proxy filing. The bank appointed her permanent successor as CRO, Kim Olson, in January of this year.

It is unclear how the bank managed risks in the interim period between the departure of one CRO and appointment of another. Representatives at SVB did not return Fortune’s request for comment.

You will be comforted knowing SVB donated $73 million to the Black Lives Matter organization (a useless entity in my opinion) and they were up-to-date on the latest Diversity, Equity, and Inclusion (DEI) policies. Perhaps they should have stuck more to banking. Have they heard the term “diversify”? Don’t put all your eggs in one basket (of T-bills)?

Hopefully, the recent run on banks will not continue. I don’t know myself where this is headed, but given this cursory look, I have doubts “experts” are focused on the right issues and that our government is advancing the right policies.

Maybe you are a financial expert. What do you think about these messes? My concern is the motivation of political leaders and the competency of so-called experts have been shown not to be so expert in their fields. Perhaps the fundamentals of our economy are strong enough to overcome their mistakes and poor political choices. I certainly hope so.

Dave https://seek-the-truth.com/about/

More links:

https://www.msn.com/en-us/money/news/what-really-broke-the-banks/ar-AA18YMpX